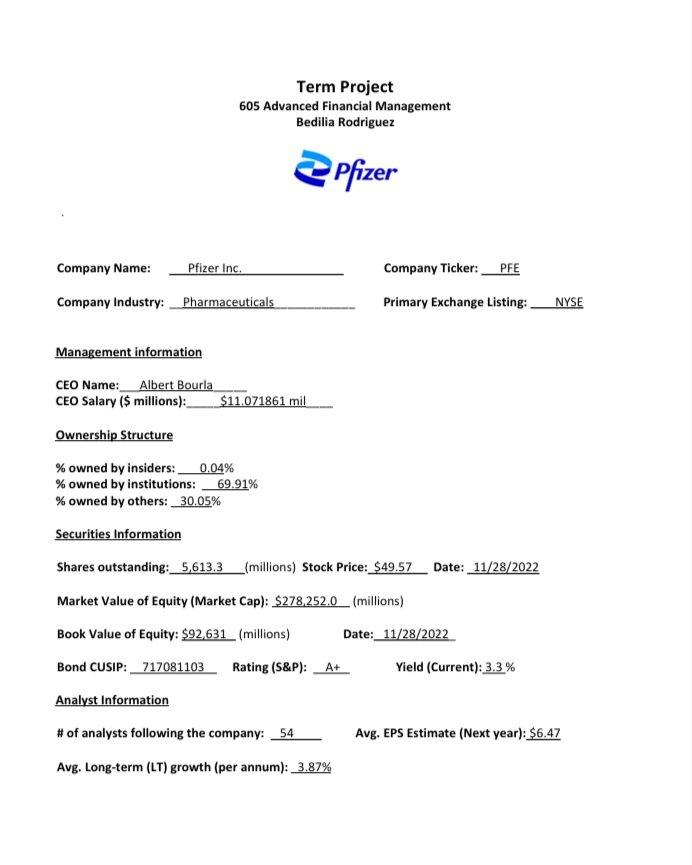

Company Valuation Analysis:

Pfizer, Inc. (PFE)

Objective: Provide stock recommendations to investors regarding Pfizer, Inc.

Analysis Conducted:

Weighted Average Cost of Capital Analysis (WACC)

Discounted Cash Flow Analysis (DCF)

Peer Company Analysis

Share Pricing

Industry Outlook

Recommendation: Buy

Pfizer has several patents in the pipeline, and one can be confident that they will be able to withstand trends that traditional investors might be averse to. As a moderate investor, one can take advantage of this situation by buying more shares in preparation for the upcoming developments.

The Debt/Equity ratio assumption at 13.3% is reasonable as it is in line with the pattern in the size of the biotech/pharma company about bigger size = lesser ratio / smaller size = higher % ratio. The risk-free rate may not be reasonable due to the uncertainty of risk of the current business activities. The corporate tax rate used may not be an accurate reflection of today’s tax rate.

A good range estimate is 7.5 to 8 as this is the range in the industry and will be at the lower risk end.

All assumptions, except the Revenue Growth rate assumption, are reasonable. Revenue assumption takes the average of the past four years' revenue growth, including an extreme 95.2% growth in the fourth year. This can be a one-time outlier event that skewed the calculations and may not be relied upon for future valuations. The 18.7% growth assumption may be overestimated. The remaining assumptions are reasonable because the historical margins are not far skewed from the assumptions and include a decrease in perpetual growth. The WACC and beta are within the industry average therefore we do not suspect high volatility.

PFE’s discount price is suspected to be a reflection of current events in relation to the consumer demand for PFE products. Specifically, -an investor’s suspected decline in the demand for the COVID-19 vaccines and other expiring patents.